Access to biologics and Janus kinase inhibitors for treatment of rheumatic diseases in the biosimilars era in Poland: a nation-level study

1 , 2, 4

Key words: biologics, biosimilars, COVID-19 pandemic, Janus kinase inhibitors, rheumatic musculoskeletal diseases

, 2, 4

Key words: biologics, biosimilars, COVID-19 pandemic, Janus kinase inhibitors, rheumatic musculoskeletal diseases

CC BY 4.0

CC BY 4.0

Access to biologics and Janus kinase inhibitors for treatment of rheumatic diseases in the biosimilars era in Poland: a nation-level study

Introduction: By reducing treatment costs, biosimilars provide an opportunity to improve accessibility to highly effective drugs.

Objectives: This study aimed to evaluate access to biologic disease‑modifying antirheumatic drugs (bDMARDs) and Janus kinase inhibitors (JAKis) among patients with rheumatic musculoskeletal diseases within a 10 year timeframe in Poland.

Patients and methods: We performed a retrospective analysis using a nationwide public payer database.

Results: By 2022, 11 102, 6602, and 4400 patients with rheumatoid arthritis (RA), psoriatic arthritis (PsA), and axial spondyloarthritis (axSpA) were treated with bDMARDs or JAKis. Peak drug utilization was observed for adalimumab, followed by etanercept and tocilizumab. Within the study timeframe, the estimated access to innovative drugs increased from 0.8%, 1.4%, and 0.8% to 3.2%, 8.7%, and 3.5% for RA, PsA, and axSpA patients, respectively. Affordable tumor necrosis factor inhibitors (TNFis) still predominate among innovative therapeutics, but their market share declined from 87% to 46%. The number of patients treated with other bDMARDs/JAKis almost doubled within the prespecified timeframe. Overall, the average annual treatment cost per patient decreased by 60%, from 7315 EUR to 2886 EUR. Despite recent safety warnings, JAKis appear to be increasingly utilized. Additional analyses regarding the COVID‑19 pandemic showed impaired access to intravenous therapies, but not subcutaneous or oral formulations.

Conclusions: In Poland, biosimilars‑related savings improved availability of higher‑priced innovative drugs rather than less costly TNFis. Data‑driven resource allocation and dedicated policy solutions facilitating access to affordable biologics are recommended.

What's new?

Biosimilars contribute to meaningful savings for health care systems in Europe. Despite this, disparities in access to affordable biologics and overall innovative treatments still exist. Data on whether allocation of the saved funds is the most beneficial from the patients’ perspective are missing. This nationwide study provides a multilevel analysis of access to innovative therapies in rheumatic musculoskeletal diseases (RMDs), with less costly tumor necrosis factor inhibitors (TNFis) serving as a benchmark. Within the study timeframe, access to biologic disease‑modifying antirheumatic drugs (bDMARDs) / Janus kinase inhibitors (JAKis) increased, but it still remains relatively low. Less expensive TNFis are still predominant, resulting in a 60% reduction in average annual treatment costs. As compared with affordable TNFis, the increase in the number of patients treated with other bDMARDs/JAKis doubled, and was responsible for spending a vast majority of funds allocated to RMDs. Policy should be developed to increase the number of bDMARD users, with reinvestment into reimbursement of less costly and other innovative agents at least to the same extent.

Introduction

Rheumatic musculoskeletal diseases (RMDs), including rheumatoid arthritis (RA), psoriatic arthritis (PsA), and axial spondyloarthritis (axSpA), represent a major challenge from a socioeconomic and health care perspective.1-3 Timely diagnosis, stringent disease control, and effective treatment are crucial steps in preventing disease‑related disability. Access to synthetic and biologic disease‑modifying antirheumatic drugs (bDMARDs) has changed a natural course of inflammatory arthritis,4 including extra‑articular manifestations,5 and has extended the possibility to improve quality of life through goal‑directed therapy.6,7 High effectiveness of biologic drugs, marked by a remarkable reduction of inflammatory symptoms, limited disease progression, including joint damage, and improved physical function, makes them a pillar of standard therapies. The steroid sparing effect and avoiding complications associated with chronic steroid use are the other important benefits for the patients.6 However, a high degree of clinical and immunologic variability is observed within all major arthritides, which translates into different patient phenotypes that may not respond to more widely available therapies. Equalized access to different treatment modalities that target various cytokine hinge points is thus crucial in attaining and maintaining low disease activity on the population level.8-10

Extending access to more novel therapeutics among patients with inadequate response to conventional treatment carries several considerations on the economic and health care levels. Due to initially high basic prices of innovative therapies in RMDs, access is driven largely by country welfare.11 Despite an advent of biosimilars and their wide endorsement by expert bodies in Europe, access to some of the older innovative drugs (eg, first‑generation biologics) is still limited in low- and middle‑income countries. To a certain degree, this may be driven by local policy regarding savings reinvestment and resource allocation.12 Recently, a paradigm shift can be observed regarding the market price of several bDMARDs due to a competition between originators and biosimilar agents. Countries with high market penetration of biosimilars (policy driven) may achieve substantial improvements in drug access through price competition and structured savings reinvestment.13 While the market uptake and competitor adaptation of adalimumab (ADA), etanercept (ETN), and infliximab (INF) are high in Europe and Canada, the United States setting has remained largely unchanged until recently.14,15

Despite good assimilation of biosimilars in Poland, access to biologic treatment in rheumatology, but also for other indications,16 is not satisfactory. In our previous report,12 we showed that savings associated with access to TNF inhibitor (TNFi) biosimilars did not result in a meaningful increase in the number of patients using these less costly bDMARDs. However, it is unknown whether the generated savings increased access to other innovative drugs within the rheumatology sector or had no relevant impact on the availability of biologics and Janus kinase inhibitors (JAKis) in rheumatology. The conditions for access to reimbursed bDMARDs and JAKis in Poland are strictly defined. They are only available in hospitals and hospital‑based outpatient clinics as part of drug programs, not in retail pharmacies. Although the treatment is free for patients, systemic limitations, for example, a degree of treatment financing by the public payer and a limited number of medical professionals in hospitals vs the number of patients requiring therapy mean that actual access to these drugs is highly limited. It almost solely depends on the drug policy of the Ministry of Health and the National Health Fund (NHF), the only regulator and payer in Poland.

The aim of this study was to evaluate access to all biologic treatments and targeted synthetic drugs during the era of biosimilar market competition in RMDs, along with their cost analysis in Poland.

Patients and methods

Study design and patient population

A retrospective analysis of patient access to bDMARDs and JAKis in Poland was conducted using real‑world data from the public payer database covering the years 2013–2022. We examined information for a total of 22 104 adult patients with RMDs undergoing treatment with ADA, ETN, INF, certolizumab pegol (CZP), golimumab (GOL), rituximab (RTX), tocilizumab (TCZ), secukinumab (SEC), ixekizumab (IXE), tofacitinib (TOF), baricitinib (BAR), and upadacitinib (UPA). For ADA, ETN, and INF, the data covered all products with the same active substance, including a reference medicine and available biosimilars. For TCZ, the data included both intravenous (TCZiv) and subcutaneous (TCZsc) formulations, which, depending on the analysis, are shown separately (as TCZiv and TCZsc) or together for both forms (as TCZ).

The analysis period covered market availability of INF (from 2014), ETN (from 2016), and ADA (from 2019) biosimilars with evaluation of savings for the public payer in Poland based on the previously described methodology.12 Data on the total number of patients and the number of patients with RA, PsA, and axSpA (including ankylosing spondylitis [AS] and nonradiographic axial spondyloarthritis [nr‑axSpA]) using bDMARDs or JAKis, as well as relevant cost analyses included the years from 2013 to 2022. Detailed treatment analysis for individual drugs was performed between 2016 and 2022. Both unified (entire RMD population) and indication‑based (RA, PsA, and ax‑SpA) analyses were performed.

Study setting

In 2013, the patients with RMDs in Poland had access to ADA, ETN, INF, and RTX. By 2016, the following drugs were reimbursed in RA: ADA, ETN, INF, CZP, GOL, TCZiv, and RTX. For PsA and axSpA patients, ADA, ETN, INF, and GOL were available. Within the following years, other novel therapies became accessible for the patients with RA, PsA, and axSpA. However, for axSpA, which includes both AS and nr‑axSpA, not all drugs were equally available. In some cases, the number of patients treated in the first year of reimbursement was too low to visualize.

Treatment access in rheumatic musculoskeletal diseases

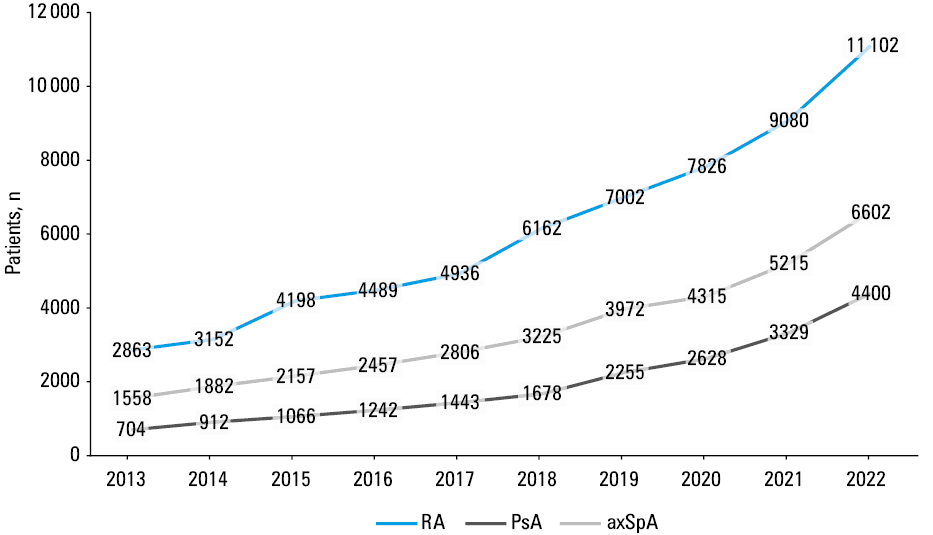

The number of patients using specific drugs for each indication was calculated. The primary analysis covered the total number of patients using bDMARDs or JAKis in RA, PsA, and axSpA (Figure 1).

The availability of bDMARDs or JAKis in RMDs in Poland was estimated using data on the number of patients treated and shown as the percentage of patients with RA, PsA, and axSpA. These data are presented with respect to the total population of patients with a given diagnosis and those eligible for treatment (Table 1). Based on epidemiologic data,17-20 the population of patients with RA, PsA, and axSpA (AS and nr‑axSpA) in our analysis has been conservatively estimated at approximately 582 500 in total, and 342 000, 50 500, and 190 000 for each indication, respectively. We assumed that the patients eligible for future bDMARDs or JAKis represented between 40% to 60% of the specific RMD population, and this estimate is based on treatment effectiveness reports.21,22

Disease | Parameter | 2013 | 2016 | 2019 | 2022 |

Absolute and relative (in relation to the total and eligible population) counts are provided for patients treated with biologic disease‑modifying antirheumatic drugs and Janus kinase inhibitors for rheumatoid arthritis (RA), psoriatic arthritis (PsA) and axial spondyloarthritis (axSpA). Eligible population estimates (eg, patients with inadequate disease control under standard care) were calculated as 40% to 60% of the total value. | |||||

RA | Treated patients, n | 2863 | 4489 | 7002 | 11 102 |

Total population | 342 000 | ||||

% of total population | 0.8 | 1.3 | 2 | 3.2 | |

Eligible population | 205 200–136 800 | ||||

% of eligible population | 1.4–2.1 | 2.2–3.3 | 3.4–5.1 | 5.4–8.1 | |

PsA | Treated patients, n | 704 | 1242 | 2255 | 4400 |

Total population | 50 500 | ||||

% of total population | 1.4 | 2.5 | 4.5 | 8.7 | |

Eligible population | 30 324–20 216 | ||||

% of eligible population | 2.3–3.5 | 4.1–6.1 | 7.4–11.1 | 14.5–21.8 | |

axSpA | Treated patients, n | 1558 | 2457 | 3972 | 6602 |

Total population | 190 000 | ||||

% of total population | 0.8 | 1.3 | 2.1 | 3.5 | |

Eligible population | 114 000–76 000 | ||||

% of eligible population | 1.4–2 | 2.2–3.2 | 3.5–5.2 | 5.8–8.7 | |

Budget impact and treatment cost analysis

Based on the public payer data, reimbursement expenditures for bDMARDs and JAKis were analyzed for RMDs (including RA, PsA, axSpA, but also pediatric population with juvenile idiopathic arthritis [JIA]). Total payer expenses covering reimbursement of all therapies, for all indications, are shown for individual years. Real‑life savings for the public payer, as described in a previous study,12 were calculated based on the total annual drug budget during the biosimilar market competition era. Savings of the public payer were calculated for the years 2019–2022 and compared with 2018, when the expenditure reached its peak value. The presented data cover all clinical indications and drugs within the RMD sector.

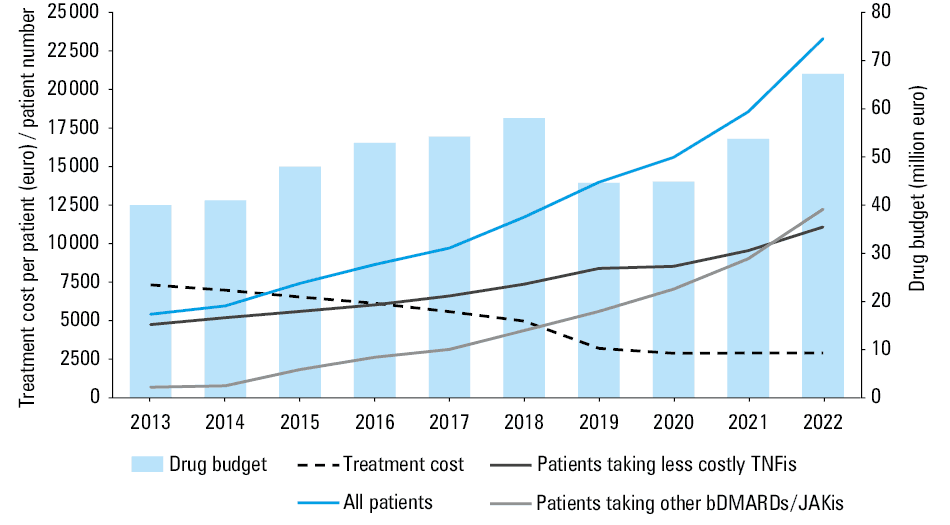

The average treatment cost per patient per year was calculated based on the total number of patients with RMDs treated with bDMARDs or JAKis. Similarly, a total reimbursement budget covering all drugs across all clinical indications was calculated. Additionally, the total number of patients treated and the number of patients in specific groups were shown (Figure 2). Data for pediatric indications are supplementary to the comprehensive nature of this analysis. All cost data are based on final drug prices, that is, they reflect the actual costs for the public payer.

Abbreviations: TNFis, tumor necrosis factor inhibitors

Individual drug utilization and distribution

Data on the number of patients with RMDs using specific therapies are reported together (Supplementary material, Figure S1) and separately for each of the analyzed clinical indications (Figure 3).

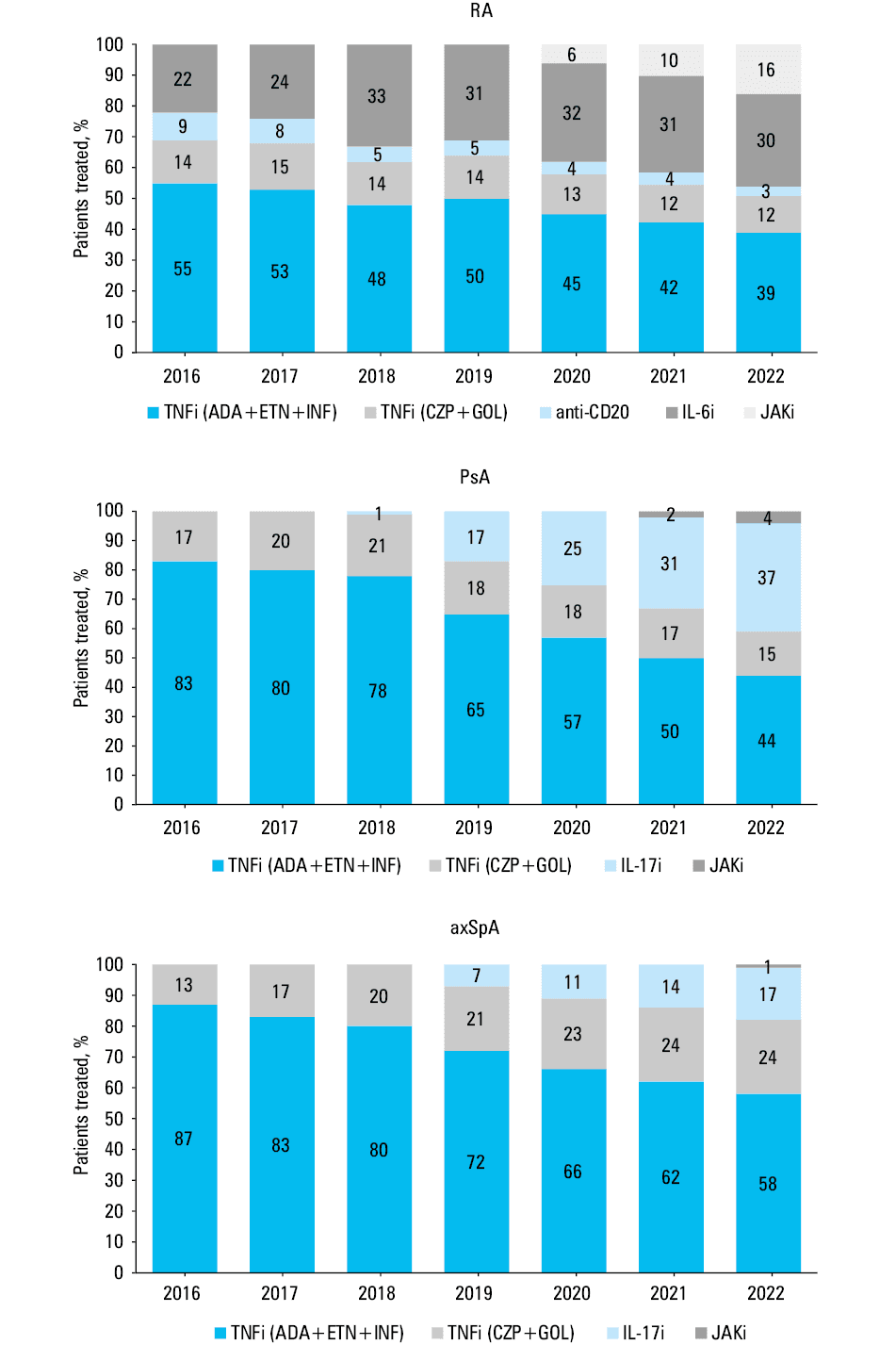

![Proportion of patients with rheumatoid arthritis (RA), psoriatic arthritis (PsA), and axial spondyloarthritis (axSpA) using affordable tumor necrosis factor inhibitors (TNFis; adalimumab [ADA], etanercept [ETN], and infliximab [INF]) vs other TNFis (certolizumab pegol [CZP] and golimumab [GOL]) and drugs with other modes of action: anti-CD20 monoclonal antibody (rituximab [RTX]), interleukin (IL)-6 inhibitor (tocilizumab [TCZ]), IL-17 inhibitors (secukinumab [SEC], ixekizumab [IXE]), and Janus kinase inhibitors (JAKis; tofacitinib [TOF], baricitinib [BAR], upadacitinib [UPA]) in Poland between 2016 and 2022](/paim/_next/image/?url=https%3A%2F%2Fpamw.pl%2Fsites%2Fdefault%2Ffiles%2Fjson_zip_files%2Funcompressed%2F16655%2FIMAGES%2FKP_WEB__FIG_03.png&w=3840&q=75)

Based on the number of patients treated, the market share of individual treatment types for RA, PsA, and axSpA was determined, with particular emphasis on TNFis (Figure 4). The drugs were grouped according to their mechanism of action into TNFis (ADA, ETN, INF, CZP, GOL), interleukin (IL)-6 inhibitors (TCZ), anti‑CD20 monoclonal antibodies (RTX), IL‑17 inhibitors (SEC, IXE), and JAKis (TOF, BAR, UPA). The group of TNFis was additionally divided into 2 subgroups of less costly TNFis (ADA, ETN, INF) and other TNFis (CZP, GOL). An absolute increase in the use of each of the analyzed groups was also shown.

Impact of the COVID‑19 pandemic on access to treatment

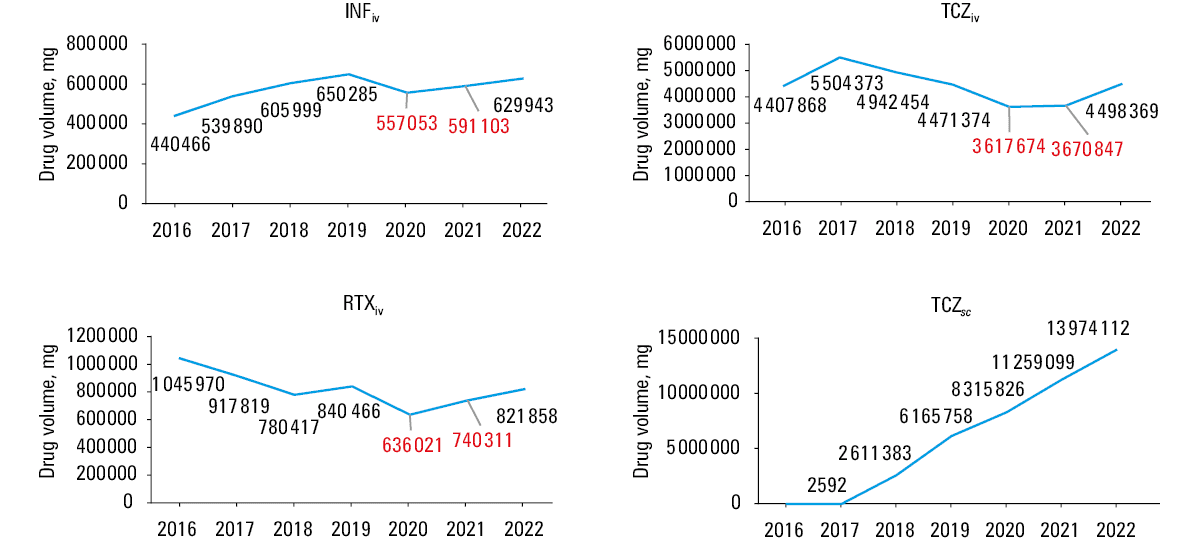

Additionally, we examined drug volume (mg) per annum to evaluate the potential impact of the COVID‑19 pandemic on temporal trends in patient access to individual therapies. Drug consumption was compared with the year 2019, before the lockdown and social isolation measures were instituted, and 2022 when the restrictions were lifted. This timeframe included a period of the strictest policy, including restriction of hospital access for patients with chronic diseases (in Poland between 2020 and 2021) (Figure 5).

Data source

Data on the annual number of patients treated and the number of drug units were sourced from the NHF Council resolutions and the NHF Statistics portal.23,24 Data on the drug budget for individual years were calculated from contract details between hospitals and the public payer.25 The source raw data are publicly available. Currency conversion was based on average euro (EUR) exchange rates in the last 5 years (1 EUR = 4.4124 PLN).

Results

Treatment access in rheumatic musculoskeletal diseases in Poland (2013–2022)

The total number of patients with RMDs treated with bDMARDs or JAKis in Poland increased by 16 979 in the analyzed period (22 104 vs 5125; 4.3‑fold), with the growth of 8239 in RA (11 102 vs 2863; 4‑fold), 3696 in PsA (4400 vs 704; 6.2‑fold), and 5044 in axSpA (6602 vs 1558; 4.2‑fold) (Figure 1).

In the total population of patients with RA, PsA, and axSpA, the access to bDMARDs or JAKis increased from 0.8%, 1.4%, and 0.8% to 3.2%, 8.7%, and 3.5%, respectively. When considering the eligible population of patients with RA, PsA, and axSpA following the prespecified conservative assumption, treatment access in these diseases in 2022 can be estimated at 6%–9%, 14.5%–21.8%, and 5.8%–8.7%, respectively (Table 1).

Budget impact and treatment cost analysis (2013–2022)

Annual drug budget and treatment cost analyses were conducted for the entire population of patients with RMDs. After reaching peak values in 2018, a successive decrease in the following 3 years was observed. Total real‑life savings of the public payer in the years 2019–2021 vs 2018 amounted to approximately 31 million EUR. In 2022, there was an increase in expenditure as compared with 2018 by approximately 9 million EUR, though the payer average annual expenditure in the years 2019 to 2022 dropped by 22 million EUR vs 2018.

Average annual treatment cost for 1 patient with an RMD decreased by 60% (from 7315 EUR to 2886 EUR). The largest decrease in average cost of the therapy was observed in 2019, which is also the year when the first ADA biosimilars were reimbursed. Throughout 2020, the cost of the therapy remained stable, and then slightly increased in the years 2021 and 2022, as compared with 2020. The rise in the number of patients treated with other bDMARDs or JAKis (vs less costly TNFis) doubled, which was responsible for the increase in expenditure in 2022 (as compared with 2018) (Figure 2).

Individual drug utilization and distribution (2016–2022)

The largest increase in drug utilization across all clinical indications was observed for ADA (+3218 patients), followed by TCZ (+2300 patients), and SEC (+2263 patients) (Supplementary material, Figure S1). When grouping the agents, the largest increase was observed for less costly TNFis (ADA, ETN, INF; +4439 patients), followed by the other TNFis (CZP, GOL; +2452 patients), IL‑6 inhibitors (+2300 patients), IL‑17is (+2735 patients), and JAKis (+2037 patients). The number of anti‑CD20 therapy users decreased by 48 patients. Overall, for TCZ, the observed increase in the number of patients was largely derived from an increase in TCZsc users (+2484 patients), with a slight decrease in the use of TCZiv (–184 patients).

In 2022, the highest consumption of biologics among RMD patients was observed for ADA (6162 patients), followed by ETN (3580 patients), TCZ (3278 patients), SEC (2263 patients), and GOL (2194 patients). Among JAKis, the largest number of patients were treated with BAR (893). Among RA patients, TCZ was the most common agent (3278 patients), followed by ADA (2351 patients), and ETN (1913 patients). For PsA, the patients treated with ADA (1398) and SEC (1205) were the most numerous. axSpA was mainly treated with ADA (2413 patients), followed by ETN (1219 patients) and SEC (1058 patients) (Figure 3).

Overall, within the entire RMD population, the share of patients taking the less costly TNFis (ADA, ETN, INF) decreased from 69% in 2016 (87% in 2013) to 46% in 2022, when comparing with other drugs. In the patients with RA, PsA, and axSpA, the respective share was 39%, 44%, and 58% in 2022, as compared with the initial 55%, 83%, and 87%, respectively. The decrease in the share of ADA, ETN, and INF in the treatment of patients with RA was caused by a significant rise in the number of patients treated with TCZ and JAKis, and in the case of PsA and axSpA, mainly by the elevated share of IL‑17is (Figure 4).

Impact of the COVID‑19 pandemic on access to treatment

The COVID‑19 pandemic and resulting lockdown imposed restrictions on inpatient care, which may have had an adverse impact on the availability of intravenous treatments. Drug consumption data for INF, RTX, and TCZiv indicate reduced consumption between 2020 and 2021, as compared with 2019 (Figure 5). A temporary nature of this decline (likely related to limited access to medical care) is reflected by drug volume changes for the analyzed therapies in 2022, with shifts to a similar (INF and RTX) or even higher (TCZiv) level than in 2019. A slight decrease in consumption was also reported for ETN, but no decrease was observed for the other subcutaneous or oral therapies (detailed data available upon request), including TCZsc. The witnessed drop in drug volume for intravenous drugs between 2020 and 2021, with a successive increase in 2022, does not correspond to the number of patients treated. This may indicate a temporary suspension of INF, RTX, and TCZiv administration for some patients due to the strictest social restrictions during the COVID‑19 pandemic.

Discussion

This retrospective study examined a 10‑year timeframe following biosimilar introduction and provided a multilevel analysis of bDMARD/JAKi availability, broken down into specific clinical indications. This is a nation‑level case study of health care system performance, in a country with very low baseline access and high baseline prices of the drugs. We compared the market share of specific therapeutic agents in RMDs using a pragmatic approach, with the less costly TNFi group treated as a benchmark. Temporal changes in average treatment price per patient and respective drug budget were examined following biosimilar introduction, as we attempted to quantify the “biosimilar effect.” Data sourcing for this study was based on the public payer reports, with near complete population coverage regarding health care claims, which enabled a reliable and robust analysis.

We showed that the total amount of adult patients treated with bDMARDs or JAKis in Poland has increased within the last 10 years over 4 times, up to over 22 000 patients. The patients with RA are the largest group, representing about 50% of the population, followed by axSpA (about 30%), and PsA (about 20%) individuals. Overall, if we consider all patients with the formerly mentioned RMDs, innovative therapies are accessible to only 4% (3.2% for RA, 3.5% for axSpA, and 9% PsA) of the total population with inflammatory arthritis. However, this approach may be flawed due to the chosen denominator, and this estimate was recalculated assuming that the patients with inflammatory arthritis and inadequate response to conventional DMARDs are the target population. With a conservative assumption that 40%21,22 of the RMD population are potential candidates for future bDMARDs/JAKis, treatment availability can be estimated at 9% for RA and axSpA and 22% for PsA patients, all of whom do not meet treatment goals during a standard therapy.

We found out that among innovative therapeutics, ADA is the preferred agent of choice, followed by ETN and TCZ. However, this depends on the underlying primary condition, with ADA, ETN, and SEC utilized mainly in PsA and axSpA, and TCZ in RA. If we compare the groups of drugs based on their mechanism of action, TNFis remain at the forefront of all clinical indications. This is not surprising, considering their clinical performance (with excellent long‑term safety and efficacy), long market presence, and high degree of provider familiarity with these agents. Of note, novel therapies are willingly adopted by health care providers in Poland, with a clearly growing trend in their utilization within the recent years. Apart from TCZ in RA, this applies to IL‑17 inhibiting agents in PsA and axSpA. Furthermore, despite recent safety warnings6 and the shortest market presence, JAKis appear to be frequently utilized (particularly in RA).

In a comparative cost analysis, the rate of less costly TNFi utilization is an important benchmark to understand the systemic strategy of resource allocation for RMD treatment. When comparing the rate of affordable TNFi utilization between 2013 (87%), 2016 (69%), and 2022 (46%), a marked decline can be observed, which is reflected by increasing accessibility of other therapeutic agents. Among RA patients (for whom novel agents are usually first accessible), the rate of affordable TNFi utilization was only 55% in 2016, as compared with the PsA (83%) and axSpA (87%) patients. By 2022, it was estimated to decline to approximately 40% for RA and PsA and 60% for axSpA. A shift toward on‑patent, higher priced therapies has also been observed in other European countries following TNFi biosimilars market entrance,26 which could be derived from improved awareness and education regarding on‑patent drugs, but also from a natural evolution and cumulative uptake of new treatment standards for patients with RMDs.27

It should be noted that although the choice of particular agents in sequential therapy for RMDs in Poland depends on the attending physician, the market share of the less costly agents remains high. The current setting allows for considerable savings for the public payer. We previously demonstrated that following biosimilar market entrance, real‑life savings for the public payer amounted to over 107 million EUR. The changes were the most dynamic between 2019 and 2021, when a net benefit amounted to 93 million EUR. If all these funds were reinvested, over 45 000 patients with RMDs could have benefited from the analyzed TNFis in 2022.12 Our study extended these findings by considering the reimbursement cost of all available agents (not only ADA, ETN, and INF), calculating the exact net savings between 2019 and 2021 and comparing drug- and indication‑specific allocation. Considering a total current 31 million EUR in net savings, close to 62 million EUR out of the previously reported savings within this timeframe were reinvested into funding novel therapeutics (on‑patent bDMARDs and JAKis).

Between 2013 and 2022, the number of patients using the less costly TNFis and other bDMARDs/JAKis rose by 6336 and 11 558, respectively. In the years 2018–2022, corresponding to the period of the greatest savings generated by biosimilars (especially ADA), the exact increase in the use of affordable TNFis and other bDMARDs/JAKis was 3706 and 7882, respectively. The average annual treatment cost with ADA, ETN, or INF in 2021 amounted to 746 EUR, 1963 EUR, and 1159 EUR per patient, respectively.12 If we considered a scenario in which all these savings were reinvested into the least costly TNFis, more than 3 times more patients could have received treatment.

High uptake of less expensive drugs may lead to a reduction in the overall cost of therapy. In Norway, between 2010 and 2019, the estimated mean annual treatment cost per RA patient declined by 47%, while for bDMARD/JAKi‑naive patients estimates indicated a nearly 75% reduction.28 We observed that the average annual treatment cost per an RMD patient declined by about 60% (from 7315 EUR to 2886 EUR) between 2013 and 2022, which is likely driven by a high share of affordable TNFis in the treatment schemes. Within the recent years, the mean cost of RMD treatment has remained relatively stable, as downward drug repricing (particularly of ADA and ETN) does not balance the growing market share of more expensive drugs. While resource reallocation into novel therapeutics is beneficial for RMD patients, it is necessary to consider how to optimize the regulatory framework of resource reinvestment. From a population perspective, increasing access to the less costly therapies is preferable in a scenario of low baseline accessibility, with additional gains obtained through achieving therapy goals early on and reducing indirect costs of illness.29-32 Once a predetermined access threshold is reached, fund reallocation toward equalized access to different therapeutic modalities may be performed. While tentative and dependent on market dynamics, devising such a policy seems warranted.

While the Polish criteria for bDMARD and JAKi treatment of PsA and axSpA are in line with the European Alliance of Associations for Rheumatology and Assessment of SpondyloArthritis International Society guidelines,33,34 high disease activity, rather than moderate, remains a requirement for RA treatment implementation. Recently, the National Institute for Health and Care Excellence approved funding of affordable TNFis in the RA patients with moderate disease activity.35 Similar policy changes are warranted in Poland and recommended by local expert bodies.

Geographic and ethnic disparities in the access to novel therapies have been previously described,11,36,37 with some reports identifying an association between nationality, biologic access, and disease activity.38 Analyses from the multinational METEOR registry39 have demonstrated that socioeconomic status is a significant factor affecting disease activity, with country welfare, regulations regarding prescription, and stringency of reimbursement affecting bDMARD availability, which is consistent with other studies.40 While increased accessibility for lower‑income residents remains achievable, the actual patient benefit on a population level is largely speculative. In countries where the biosimilar switch is not mandatory but rather based on the provider’s decision, if the cost of a reference drug remains relatively high, the degree of potential savings depends on education of the provider.41 If the payer is public rather than private, illness cost modelling with cost‑effectiveness breakdown of a given medication is likely to be a major driver of the payer decisions. Studies have demonstrated that biosimilar use in the United States setting is limited, which may reflect a low amount of data regarding biosimilar equivalence and switch effectiveness.42,43 A knowledge gap among providers may be another issue, as familiarity and terminology could play a role in choosing the agent.44,45 It should be emphasized that projecting savings associated with biosimilars entrance on the United States market depends on changing regulatory structure and insurer’s calculations.46-48

Policy changes toward extending access to innovative treatment should also consider patient‑level factors, with potential preference for oral or subcutaneous formulations. The inclusion of the COVID‑19 pandemic within the study timeframe provided us with a unique opportunity to examine real‑life changes in access to drugs associated with health care system restrictions and self‑isolation behaviors. Intravenous admission rates are subject to greater provider dependency, which may lead to treatment discontinuation due to external factors. Data from Canada indicate that disease activity in RA patients remained stable during the COVID‑19 pandemic, with high persistence in bDMARD therapy and a significant increase in JAKi use.49 In the present study, we have shown impaired adherence to intravenous biologics following implementation of pandemic‑driven restrictions, specifically in the initial stages, where inpatient care was more difficult to access. We did not observe such an effect for subcutaneous and oral drugs, the availability of which also depends on institutional health care but is outpatient‑based in Poland.

Given the potential future restrictions and most favorable rates of long‑term disease control in TNFi persisters,50 subcutaneous affordable TNFis appear the preferred agents for the general RMD population. In specific cases, such as young patients without adverse event risk factors, JAKis may be used as clinical equivalents.51

Strengths and limitations

The major advantage of this analysis is to show a full impact of biosimilars introduction on the access to all innovative treatments in RMDs at the national level. Shaping of the health care system after the introduction of biosimilars is crucial for achieving benefits resulting from their availability at the population level. A thorough analysis of the market share of individual therapies and the annual drug budget over time indicated that an opportunity for optimal fund allocation may be lost.

Since the study was conducted using the public payer data, hypothetical limitations may result from the accuracy of data available in the NHF records; however, no relevant discrepancies across different NHF sources in relation to the number of patients and treatment costs were noted. Although data from the public payer database may not cover all cases of using the described treatments, they show all patients treated under health insurance in Poland. The remaining patients taking the analyzed drugs can be treated thanks to private funds, but their potential number, to the best of our knowledge, is unlikely to affect the overall study results.

It should be emphasized that the presented calculations required several assumptions. We conservatively assumed a static number of patients with RMDs, for whom sample estimates are based on a theoretical range derived from epidemiologic studies. Given the data‑driven lower and upper bound, calculations based on a stable number of patients are likely to yield a reliable estimate, while enabling easier evaluation of temporal changes in drug access. However, when reporting count and frequency data, we were unable to account for epidemiologic variations in the RMD population over time. If we consider data from the Global Burden of Disease study,52 gathered in 195 countries and covering the years between 1990 and 2017, we can observe incremental trends both in incidence (8.2%) and prevalence (7.4%) of RA. Given the current 10‑year study timeframe, potential variations in the RMD population level are unlikely to significantly affect the magnitude of changes.

Conclusions

In the Polish setting, regulatory constraints limit bDMARD prescription to a hospital‑based, specialist‑driven decisions. At the same time, regulations that would encourage the use of more affordable bDMARDs are limited, which leads to savings reallocation into enhanced access to other, higher‑priced drugs. On a population level, with relatively low access to biologic and targeted synthetic DMARDs, this has marginal effects. Policy should be developed to enhance the total number of bDMARD users through appropriate incentivizing, with reinvestment into reimbursement of less costly and other innovative agents at least to the same extent. A lesson from Poland can help other countries that are at an earlier stage of biosimilars introduction to find effective solutions and take full advantage of access to these medications.

- Scott IC, Whittle R, Bailey J, et al. Rheumatoid arthritis, psoriatic arthritis, and axial spondyloarthritis epidemiology in England from 2004 to 2020: an observational study using primary care electronic health record data. Lancet Reg Health Eur. 2022; 23: 100519. | Crossref

- Bergman MJ, Zueger P, Patel J, et al. Clinical and economic benefit of achieving disease control in psoriatic arthritis and ankylosing spondylitis: a retrospective analysis from the OM1 registry. Rheumatol Ther. 2023; 10: 187‑199. | Crossref

- Huscher D, Merkesdal S, Thiele K, et al; German Collaborative Arthritis Centres. Cost of illness in rheumatoid arthritis, ankylosing spondylitis, psoriatic arthritis and systemic lupus erythematosus in Germany. Ann Rheum Dis. 2006; 65: 1175‑1183. | Crossref

- Smolen, J, Aletaha, D, Barton, A, et al. Rheumatoid arthritis. Nat Rev Dis Primers. 2018; 4: 18001. | Crossref

- Sumida K, Molnar MZ, Potukuchi PK, et al. Treatment of rheumatoid arthritis with biologic agents lowers the risk of incident chronic kidney disease. Kidney Int. 2018; 93: 1207‑1216. | Crossref

SUPPLEMENTARY MATERIAL

ARTICLE INFORMATION